We are currently living in one of the greatest crises in history. The coronavirus has paralyzed and closed most of the businesses, partially or totally. It generated disruptions in supply chains, millions in losses, and layoffs on a global scale. In the United States alone, around 40 million people have lost their jobs. This will generate a domino effect on consumption and credit. A situation that strongly affects the cash flow and balance sheet of companies is increasingly facing challenges of efficiency and profitability to ensure their survival in the face of the crisis.

An alternative to strengthen troubled companies is to merge them with others by looking for synergies. Synergy is when the sum of the parts is higher than the elements themselves. If we put it in a numerical example, 1+1 would typically be 2. However, when there are synergies, 1+1 is greater than 2. In business terms, it would be when the merger of two companies generates a much better result in value and performance than only the sum of the individual companies.

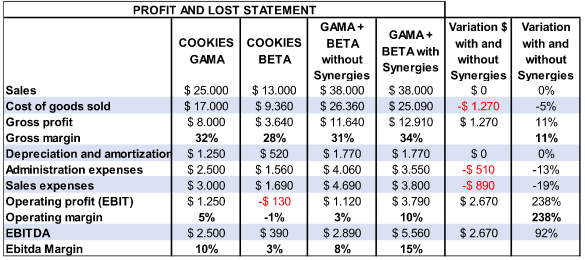

A hypothetical example

Two manufacturing companies produce cookies. The following is their profit and loss statement:

As we can see, Cookies Gama’s gross margin was 32% and Beta 28% before the merger. Gama has better margins because it has higher production volumes. Moreover, it has better use of its installed capacity, and access to raw materials at lower costs.

After the merger, without capturing productive synergies, the combined companies have a gross margin of 31%, and by capturing synergies, this margin improves by 3% to 34%.

In the next step, we present how much the administration and sales expenses weigh before and after the merger.

As one can see, before the merger, Cookies Gama had sales and administration expenses of 22% and Cookies Beta of 25%. Still, after the merger, with synergies, the new company Gama Beta has total expenses of 19%.

What kind of synergies can be achieved in consolidation processes?

Productive:

It may be that, when merging two companies, two production plants are no longer required, but only one of the existing ones, or a larger one. There may also be equipment that is used in the processes of both companies.

Purchasing:

By having higher production volumes, and using the best negotiation practices that Cookies Gama had, substantial savings are achieved in the negotiation with suppliers. It is not the same to buy 100 tons of sugar per year to buy 150.

Cross-selling:

Cookies Beta is strong selling in supermarkets, while Gama is healthy in small shops. After the merger, some Gama references can be sold in supermarkets. Some Beta recommendations in small shops, using the same vendors and vehicles for transportation. This synergy is not reflected in the previous example to make it a bit more acid, but it is feasible.

Elimination of duplicate positions:

Previously, each company had its board of directors, tax inspector, general manager, human resources manager, and production manager. In the post-merger scenario, only one person will remain in each position, and only the best employees will be selected to work in the new company. This is even though the process of dismissing some employees within the merger process may generate non-recurring extraordinary expenses.

Elimination of duplicate expenses:

Before the merger, each company had its guild subscription, paid ERP software fees, and the chamber of commerce renewal fees annually, now some of these expenses can be consolidated.

Transfer of Know-How:

Normally, some companies are more reliable in administrative processes, others in commercial or productive operations. By combining two companies, it is possible to adopt the best practices of each company, and as a result, a better-managed company is achieved.

Value creation:

Larger and more profitable companies can be sold better and are more attractive to large players active in the world of mergers and acquisitions, also for Private Equity funds. This results in achieving higher EBITDA, better margins, and much higher sales; now, the company becomes a valuable acquisition target. Before the merger, Gama had a hypothetical value of 8 times the EBITDA, ($2500 x 8 = $20,000). Beta had a value of 6 times the EBITDA ($390 x 6 = $2340). Both companies had a combined EBITDA of $2890. However, after the synergies materialized, the combined company has a value of $5560 x 8 times EBITDA = $44,480. Therefore, it generated a value of $44,480 – $22,340 = $22,140.

How is the shareholding of the new entity divided between Cookies Gama and Beta? That depends mainly on the negotiation process. It is not necessarily distributed in proportion to the value before the acquisition process. A good investment banker will help the owners of Cookies Beta to enjoy a part of the synergies.

Real synergy examples

An excellent example of exploiting synergies was the acquisition of Gillette by P&G (Procter & Gamble) in 2005. The companies expected a combined cost reduction of $1.2 billion and an increase in sales of up to $700 million over the long term. This was a result of the merger between two industry leaders¹.

In Colombia, an example of a successful business merger occurred in 2005 and 2006. Eight cement companies in the country (including Nare cement, Cementos del Valle, and Cementos del Caribe) merged (around the Caribbean cement). This merger took place using a share exchange. Cementos Argos took a 70% stake in the new company under the name of Grupo Argos². This merger put Argos on the path to international expansion. It is one of the largest producers in Latin America and the southern United States (El Tiempo).

This strategy has not been the only one. In the Antioquia business group (GEA), bank mergers such as Bancolombia, Corfinsura, and Conavi have taken advantage of synergies and economies of scale. It positioned Bancolombia as the largest bank in the country with operations throughout the region. There have also been mergers in the food sector. The merger of Noel and Zenú and Nacional de Chocolates, positioned Nutresa (formerly the national chocolate group) as one of the most successful multi-latinas in the food sector³.

Not everything is smooth within the business merger processes. Negative synergies can also occur. For example, in 1998, Chrysler and Daimler (Mercedes Benz) merged. They seeked to improve the competitiveness of both companies, but this merger never succeeded.

Some of the reasons for the business merger:

- Chrysler’s top executives in the United States had much larger compensation packages than German executives, even though Chrysler was much less profitable.

- An attempt was made to combine two companies in countries with very different languages and cultures. Culture is an intangible that plays a fundamental role that can erode a merger process.

- The Germans never wanted to share the know-how used to produce the famous Mercedes at competitive prices with the Americans out of mistrust, even though they owned Chrysler.

- Rising fuel prices in the late 1990s strongly affected Chrysler’s sales.

- Daimler did not perform proper due diligence before the acquisition. If they had, they could have avoided costly mistakes at the time of the acquisition.

Written by Simón Restrepo Barth, Partner of ONEtoONE Corporate Finance. He has a Master in Finance from Universidad de Los Andes and a certificate in advanced valuation with high honors in NYU|STERN.