An obvious objective for the seller of a company is to maximize the company’s sale price. While securing the highest price possible in an M&A deal requires the alignment of many different factors, such as market conditions, sale timing and of course speaking with motivated buyers, two related concepts that have an important impact on deal terms are value and worth. An understanding of these concepts can significantly increase the probability of a successful company sale process.

The difference between value and worth

While the words “value” and “worth” are often used interchangeably, in the financial context they mean different things. The value of an item refers to the price for an asset that a reasonable buyer and a reasonable seller would agree to. This price is generally derived by one of several commonly used valuation approaches. These include the asset approach, the market approach or the income approach. Worth is a price that a person would be willing to pay for an item regardless of what its value might be. This amount may be significantly more or less than the item’s market value.

To provide an example, the market value of a sweater may be 10 dollars. However, if you are cold you may be willing to pay much more for it. The important thing to note is that this does not mean that the value of the sweater is more than 10 dollars. It means that, at a particular time, the sweater was worth more than 10 dollars to you. If the temperature were to rise, your willingness to pay more for it than its market value would likely fall. Similarly, you may be willing to give the same sweater away for a fraction of its market value. This may be because you decided that red and blue polka dots are no longer your color scheme of choice.

Value and worth in the company sale context

Of course, concepts of value and worth are always present in company sale negotiations. In theory, both the buyer and seller should approach the issue of a company’s value from a market-derived valuation perspective, but the reality of deal negotiations is often not so straight forward.

Sellers:

At times they approach the sale of a company from the perspective of what the company is worth to them rather than what a reasonable valuation of the company would be. Of course a seller is free to value a company at any price. However, the more an expected price deviates from a market-derived valuation the harder the company typically will be to sell. Sellers can also take the opposite position, where they assume that because market conditions are difficult or the company is losing money it does not have any value. In fact, companies that are losing money can be extremely valuable, provided that they have valuable assets or strong future growth prospects.

Buyers:

Buyers also intentionally or unintentionally often confuse value and worth. When many buyers value a company they calculate the value by discounting the company’s future cash flows by the buyers’ “required rate of return”. This is just another way of saying what the asset is worth to them. Conversely, buyers may be willing to pay much more than the market valuation. If it is vital to defend a company’s current market position, give it a strong competitive advantage or for its future growth.

Value and worth in company sale negotiations

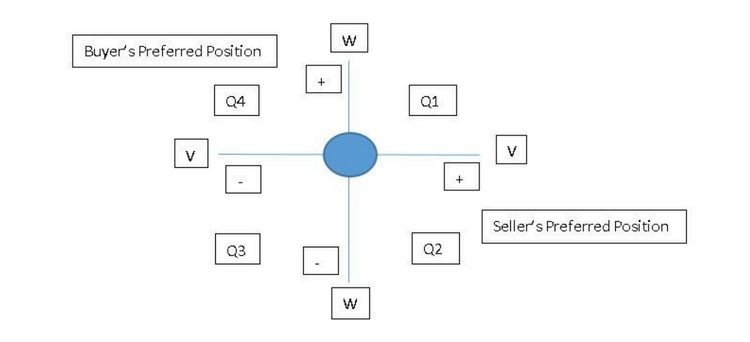

Understanding the difference between value and worth is very important in company sale negotiations. The graph shows the relationship between value and worth, buyer and seller negotiating tendencies and typical sale outcomes.

This graph outlines four potential negotiation posture quadrants, representing different possible combinations of worth and value. The preferred position of the buyer is typically in quadrant 2. Thus, the buyer receives maximum value for something that is worth little to him. The preferred position of the seller is typically quadrant 4. Here, the seller pays minimum value for something that has high worth for him. There are natural market and negotiating tendencies for sale prices to fall within the circle at the center of the graph where worth is reasonably close to price.

Value and worth and sale negotiation strategy

The four value and worth quadrants offer a key strategic lesson to sellers. Sellers should carefully search for potential buyers motivated to pay more than market-derived prices for a company or its assets. This may be because:

- the buyer benefits from favorable buying conditions, such as sudden liquidity or access to low-priced capital, that can be used to make an acquisition.

- the buyer needs to move faster than competitors to secure its market position and is willing to pay a premium for a quick deal closure.

- due to synergies between the buyer and seller, the post-acquisition value of the company will be or can be made to be greater than its current market value.

Conclusion

Successful company sale strategy and negotiation depends on many different factors. No single strategy or negotiation approach will work under all circumstances. However, being conscious of the difference between value and worth can help sellers identify buyers who are likely to pay the highest price possible.

This article was written by Darin Bifani. If you would like to know more about the difference between price and value when selling your company, take a look at The value of nothing – How to accurately calculate a company’s value.

The photo for this article was taken by Maxime Le Conte de Floris.